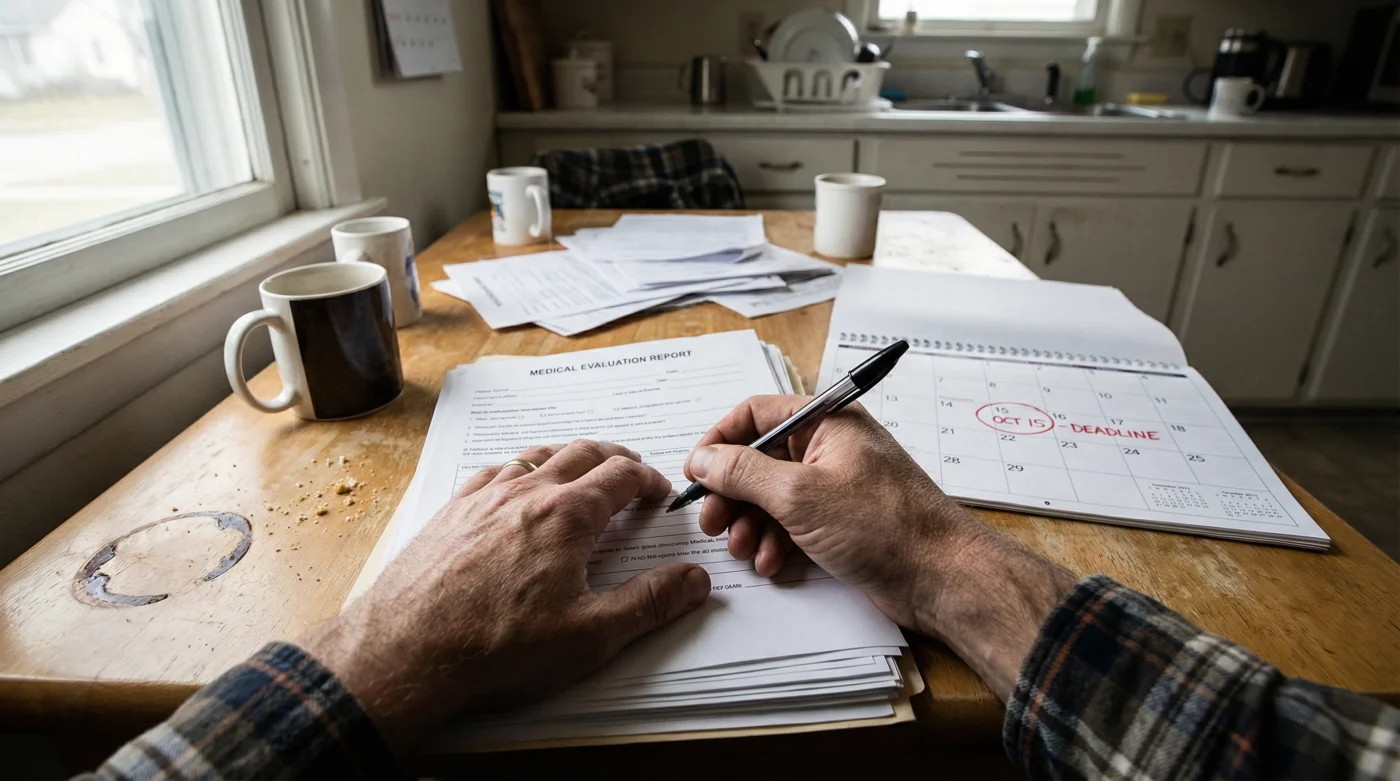

You are sitting at the kitchen table. The morning coffee has gone cold, leaving a dark, bitter ring at the bottom of the mug. Outside, the early autumn frost clings to the cedars, but inside, your attention is fixed on a stark white envelope bearing the Sun Life Financial logo. You trace the stiff edge of the paper, feeling a sudden knot in your stomach. You thought the fight was over. You submitted the absolute mountain of initial medical forms months ago, assuming that the original, exhaustive diagnosis was the final hurdle. Instead, the letter in your hands speaks of a suspended claim. The financial safety net you relied on to keep your household running has suddenly, quietly vanished.

The Myth of the Permanent Passport

You might believe that a serious diagnosis acts as a permanent passport to long-term disability coverage. It is a common, highly understandable misconception. When you are dealing with severe illness or injury, you assume the initial paperwork, signed and stamped by your physician, proves your reality once and for all. But an insurance claim is not a static document locked away in a filing cabinet; it is a living dialogue with the provider. When you skip the mandatory medical updates, you are effectively hanging up the phone mid-conversation.

The paper trail demands a continuous pulse. The rule is incredibly strict, yet rarely emphasized enough during the initial overwhelming approval process: you must provide continuous specialist documentation every 90 days. Without this crucial update, the administrative system blindly assumes your silence means a full recovery. It does not matter how permanent your condition feels to you; the paperwork must continually prove it.

| Policyholder Profile | The Common Assumption | The 90-Day Impact |

|---|---|---|

| Chronic Illness Sufferer | Condition is lifelong, making routine updates redundant. | Claim abruptly suspended due to a lack of recent symptom tracking. |

| Post-Surgery Patient | Initial surgeon report covers the entire healing year. | Benefits halt immediately if rehab progress is not documented quarterly. |

| Mental Health Claimant | Psychiatric confirmation is a one-time necessity. | Coverage dropped without continuous therapist and specialist notes. |

Meet Sarah, a former claims adjudicator who spent a decade working out of a bustling office in downtown Toronto. She knows the rhythm of these files intimately. “People treat the initial approval like a finish line,” she explains, tapping her pen against the table. “But it is really just the starting gun. We do not suspend payments because we want to punish anyone; we suspend them because the contract legally mandates recent medical evidence. If the 90-day window closes and we have not heard from a specialist, the system automatically halts the cheque.” She recalls countless Canadian families thrown into sudden financial chaos simply because they missed a routine check-in, falsely believing their severe illness spoke for itself.

| Claim Timeline | Action Required by Policyholder | Sun Life System Response |

|---|---|---|

| Day 1 to 30 | Submit initial diagnosis and Attending Physician Statement. | Claim assessment and initial approval phase begins. |

| Day 60 | Schedule follow-up appointment with treating specialist. | File flagged for upcoming mandatory medical update. |

| Day 90 | Submit updated clinical notes detailing current limitations. | Continuous coverage verified; monthly cheque issued. |

| Day 91+ (No Update) | Scramble to book emergency doctor visit to restore file. | Automatic suspension of benefits pending new medical evidence. |

Maintaining the Dialogue

How do you protect your livelihood from this administrative trap? You start by treating your medical appointments as essential financial maintenance, much like changing the furnace filter or paying your mortgage. Do not wait for Sun Life to send a reminder letter through the mail. You need to be fiercely proactive. Schedule your specialist visits well before the 90-day mark approaches. Keep in mind how agonizingly long wait times can be in the Canadian healthcare system.

When you sit in the doctor’s office, be intensely specific about your current limitations. Do not just say you are feeling about the same. Request that your specialist notes exact, measurable changes. Have them document your persistent lack of mobility, your daily pain levels on a scale, or the ongoing cognitive fatigue that prevents you from focusing. The adjudicator cannot see you; they can only read the ink on the page.

- Sun Life Financial policyholders jeopardize disability claims skipping this mandatory physician update.

- Garmin Forerunner users double battery lifespan disabling this specific ambient sensor setting.

- Volkswagen Golf drivers prevent sunroof leaks clearing this specific hidden drainage channel.

- Amazon Prime Canada is quietly enforcing minimum thresholds for standard expedited shipping.

- Quaker Oats preparers guarantee creamier textures executing this mandatory dry toasting phase.

| Documentation Quality | What To Look For (Green Flags) | What To Avoid (Red Flags) |

|---|---|---|

| Symptom Description | Specific measurements (e.g., cannot stand for more than 10 minutes). | Vague statements (e.g., patient is still unwell). |

| Treatment Plan | Documented medication changes, referrals, and active therapies. | Notes stating simply continue current treatment without any context. |

| Physician Credentials | Forms filled out by a specialized practitioner for your specific condition. | Forms completed solely by a walk-in clinic general practitioner. |

| Submission Timing | Sent 10 to 15 days before the 90-day deadline expires. | Sent on the 89th day, risking massive administrative processing delays. |

Securing Your Peace of Mind

Understanding this strict 90-day rhythm fundamentally changes how you navigate your path forward. It transforms a source of sudden, unexpected panic into a predictable, highly manageable routine. You are no longer living at the mercy of the mailbox, wondering if your next cheque will arrive to cover the groceries. You become the director of your own claim.

By taking absolute control of this continuous update cycle, you build a protective fortress around your coverage. It eliminates the blind spots that lead to sudden suspensions. This diligent preparation allows you to step back and focus on what actually matters. You can dedicate your energy to your physical health, your family, and healing at your own pace, resting easily with the knowledge that the financial floor beneath you remains solid and secure.

“Your medical file is the vital pulse of your claim; if the updates stop, the coverage flatlines.”

Frequently Asked Questions

What happens if my specialist is booked months in advance?

You must notify Sun Life immediately in writing with proof of the scheduled appointment to request a temporary extension on your file.Does a note from my family doctor count for the update?

Generally, no. Insurance providers require updates from the specific specialist treating your disabling condition for long-term claims.Will Sun Life backpay me if my claim is suspended?

Yes. If you eventually provide the missing 90-day documentation proving continuous disability, retro-payment is typically issued for the suspended months.Is the 90-day rule standard across all Canadian insurers?

While exact timelines vary slightly between companies, the requirement for continuous, regular medical evidence is a universal industry standard.Can I submit the medical forms through an online portal?

Yes. Utilizing the official Sun Life app or web portal is often faster and provides a crucial digital timestamp of your submission.